Featured

Table of Contents

Insurer will not pay a minor. Rather, think about leaving the cash to an estate or count on. For more in-depth information on life insurance coverage get a duplicate of the NAIC Life Insurance Policy Purchasers Guide.

The internal revenue service places a limit on just how much money can enter into life insurance policy premiums for the plan and how quickly such costs can be paid in order for the policy to maintain every one of its tax obligation advantages. If certain limitations are exceeded, a MEC results. MEC policyholders might be subject to tax obligations on distributions on an income-first basis, that is, to the extent there is gain in their plans, as well as penalties on any type of taxable quantity if they are not age 59 1/2 or older.

Please note that exceptional finances build up rate of interest. Revenue tax-free therapy additionally thinks the lending will become pleased from earnings tax-free death benefit proceeds. Lendings and withdrawals lower the policy's money value and death advantage, may create certain policy benefits or riders to become inaccessible and may increase the opportunity the plan might lapse.

4 This is offered with a Long-lasting Treatment Servicessm cyclist, which is offered for a surcharge. In addition, there are restrictions and restrictions. A client may certify for the life insurance policy, but not the rider. It is paid as a velocity of the survivor benefit. A variable global life insurance coverage agreement is an agreement with the main objective of giving a fatality advantage.

What is Senior Protection?

These portfolios are very closely managed in order to please stated investment purposes. There are fees and fees connected with variable life insurance contracts, consisting of mortality and danger costs, a front-end tons, administrative costs, investment management charges, abandonment charges and costs for optional motorcyclists. Equitable Financial and its affiliates do not offer lawful or tax guidance.

And that's great, because that's precisely what the death advantage is for.

What are the advantages of entire life insurance? One of the most enticing benefits of buying an entire life insurance policy is this: As long as you pay your costs, your fatality benefit will never run out.

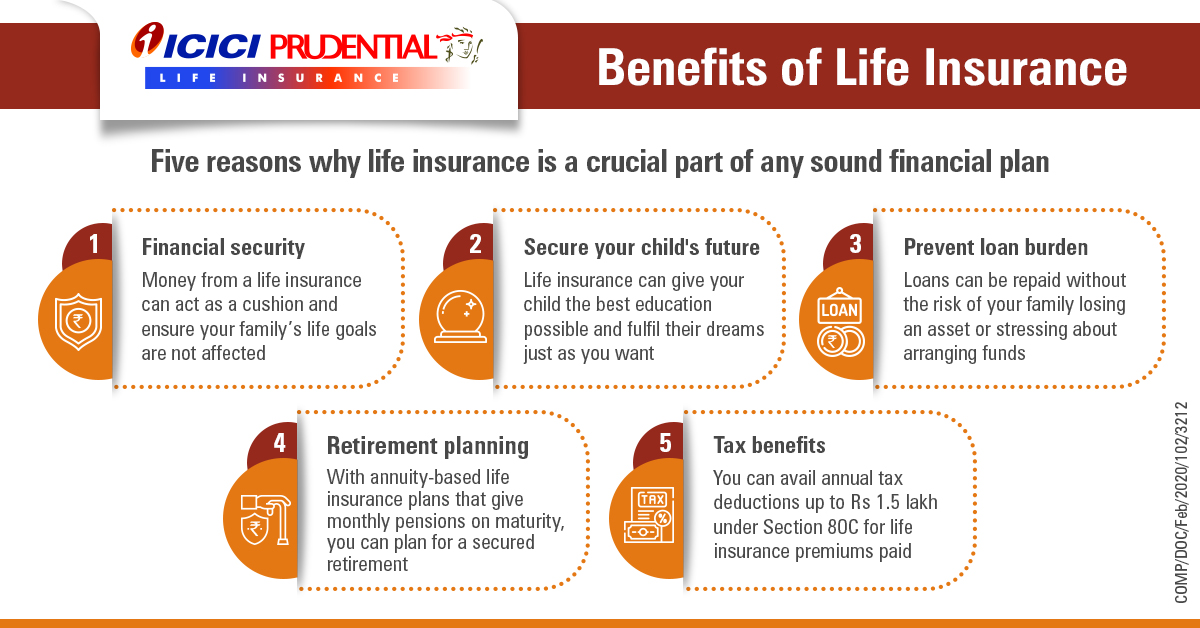

Assume you do not need life insurance if you do not have kids? You might intend to reconsider. It may seem like an unnecessary expenditure. There are several benefits to having life insurance, even if you're not sustaining a family. Here are 5 reasons you need to purchase life insurance policy.

How long does Whole Life Insurance coverage last?

Funeral expenditures, funeral costs and clinical costs can build up (Level term life insurance). The last thing you desire is for your enjoyed ones to carry this extra concern. Long-term life insurance is offered in numerous amounts, so you can choose a death advantage that fulfills your needs. Alright, this just applies if you have children.

Figure out whether term or irreversible life insurance policy is best for you. As your personal situations adjustment (i.e., marital relationship, birth of a child or work promo), so will certainly your life insurance policy requires.

Essentially, there are two kinds of life insurance policy plans - either term or long-term plans or some combination of the 2. Life insurance providers offer various forms of term strategies and typical life policies as well as "rate of interest sensitive" products which have actually ended up being much more widespread since the 1980's.

Term insurance supplies defense for a given amount of time. This period could be as brief as one year or give insurance coverage for a specific number of years such as 5, 10, 20 years or to a specified age such as 80 or sometimes as much as the earliest age in the life insurance policy mortality tables.

How can I secure Accidental Death quickly?

Presently term insurance rates are very competitive and among the most affordable traditionally knowledgeable. It should be kept in mind that it is a commonly held belief that term insurance is the least costly pure life insurance policy protection available. One needs to evaluate the plan terms thoroughly to make a decision which term life options are appropriate to satisfy your certain conditions.

With each new term the premium is enhanced. The right to renew the plan without proof of insurability is an essential advantage to you. Or else, the threat you take is that your health might weaken and you may be not able to acquire a plan at the same prices or perhaps at all, leaving you and your beneficiaries without coverage.

You need to exercise this choice throughout the conversion period. The length of the conversion duration will vary relying on the kind of term policy purchased. If you transform within the prescribed duration, you are not called for to offer any info about your health. The costs price you pay on conversion is generally based on your "present obtained age", which is your age on the conversion day.

Under a level term policy the face amount of the plan continues to be the very same for the entire duration. With reducing term the face amount decreases over the period. The costs remains the very same every year. Frequently such plans are marketed as home mortgage security with the amount of insurance coverage decreasing as the balance of the mortgage reduces.

Who offers Accidental Death?

Typically, insurance providers have not deserved to transform costs after the plan is offered. Since such plans may continue for several years, insurance providers need to use conventional mortality, interest and expense price price quotes in the costs estimation. Flexible premium insurance, nevertheless, permits insurers to provide insurance coverage at reduced "present" premiums based upon less conservative presumptions with the right to change these premiums in the future.

While term insurance is made to supply defense for a specified amount of time, irreversible insurance policy is developed to supply protection for your entire life time. To maintain the costs price degree, the premium at the younger ages exceeds the actual cost of security. This additional premium constructs a book (cash money value) which aids pay for the plan in later years as the expense of defense increases above the costs.

The insurance policy business invests the excess premium dollars This type of plan, which is often called cash money worth life insurance coverage, produces a financial savings element. Cash worths are vital to a long-term life insurance policy.

{kind=link}

Latest Posts

Burial Insurance Plans

Final Expense Company

Average Cost Of Final Expense Insurance